Investing in Czech real estate

Located in the heart of Europe, the Czech Republic is the right choice when you are looking to invest in commercial property. The country remains an attractive option for new investors due to its open investment climate with political and economic stability, existing research and development platforms and safe and secure business environment.

Investment opportunities

In 2025, the Czech commercial real estate investment market rebounded strongly, led by a surge in large-ticket deals and broader activity across all major segments. In Q1 the total investment volume reached about €1.7 billion, boosted by the sale of Contera's industrial portfolio, the biggest logistics transaction since the pandemic. Hotels and prime retail also played a major role, withthe Prague Hilton deal and landmark retail assets such as Myslbek or Atrium Flora changing hands. Domestic capital continued to dominate overall, accounting for roughly two-thirds of investment volume, with US investors contributing around one quarter. Market sentiment significantly improved.

Industrial sector

In 2025, the Czech industrial real estate market saw increased tenders, especially for automotive and consumer goods storage, with a slight rise in rents and demand. Developers remained flexible, offering incentives and short-term leases, while subleases were common. E-commerce continued to grow, but uncertainty from geopolitical tensions and potential trade wars affected demand. In Q2, major players strengthened their positions, while Chinese e-shops disrupted competition. Logistics providers improved capacity, and tenders increased, often driven by foreign investors. Demand for higher technical standards in warehouses grew, even at higher rents. Sublease supply decreased, regional rent differences widened, and there was a shortage of large ready-to-build projects near Prague.

Retail sector

Czech retail market in 2025 was dominated by retail parks, which delivered over 40k sq m of new space in total (from new schemes and extensions), while shopping centres also regainedmomentum and broadly kept pace through major refurbishments and renewed supply activity (notably Forum Pardubice and Kotva). By year-end positioning, around 200k sq m was underconstruction or renovation, with shopping centres representing over half of that pipeline, signalling a fairly balanced development outlook. Demand stayed strong, reflected in the entry of 16 newbrands mainly from fashion and gastronomy, concentrated largely in Prague.

Office sector

The Prague office market in 2025 is defined by very limited new development, declining vacancy and strong demand — particularly from the IT sector. This continues to push rents upward, especially in the city centre, strengthening landlords' position, while companies increasingly seek flexible and sustainable workspace solutions. The market is stabilising with a clear shift towardquality and ESG, but the restricted supply creates short-term competitive pressure on tenants. New construction remains insufficient to meet medium-term demand, which accelerates pre-leasing activity in prime projects. At the same time, renegotiations stay high as companies aim to secure favourable terms before further rental growth.

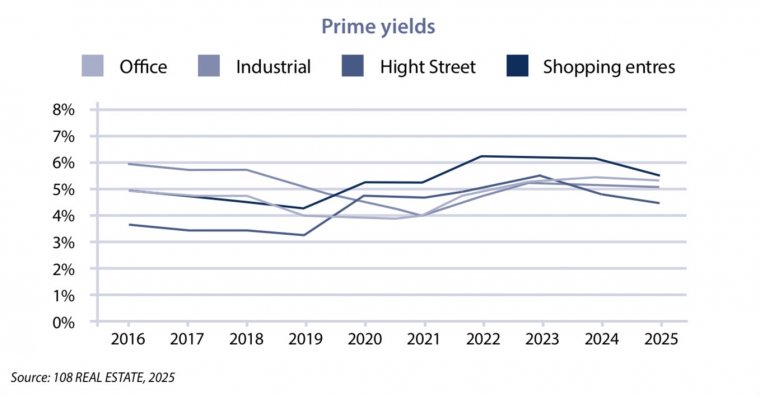

Prime yields

|

Jakub Holec, MRICS, SIOR |

|