Dealmaking in Czechia: Key Trends in Share Purchase Agreements for 2026

In today's dynamic M&A landscape across Central Europe, understanding the evolving trends in Share Purchase Agreements (SPAs) is essential for successful dealmaking. How are transaction structures shifting, what risk allocation mechanisms are gaining prominence, and which protective clauses are becoming market standards as we approach 2026?

Introduction

This article examines main trends in M&A deals and their terms embedded in Share Purchase Agreements from major transactions dealing with 100% ownership interest in companies. Our recent analysis conducted in Central Europe based on data from the past three years offers insights into how transaction structures, risk allocation, and protective provisions have evolved in response to changing market conditions across the Central Europe. Trends in the Czech M&A market closely align with regional patterns, as key Czech market players are actively engaged throughout the broader region.

Evolving SPA Trends in Central Europe and Czechia

The Central European and Czech M&A market has undergone significant transformations since 2022, reflecting broader geopolitical and economic changes. Following periods of uncertainty caused by the Covid pandemic and broader geopolitical tensions, dealmakers have adapted their approaches to transaction structures and risk allocation. This evolution is particularly evident in the components of Share Purchase Agreements, where several shifts have emerged.

Our analysis of major share-deal transactions across 14 Central European jurisdictions reveals significant changes in key SPA provisions compared to previous years. These insights offer valuable benchmarks for companies engaging in M&A activities in the region.

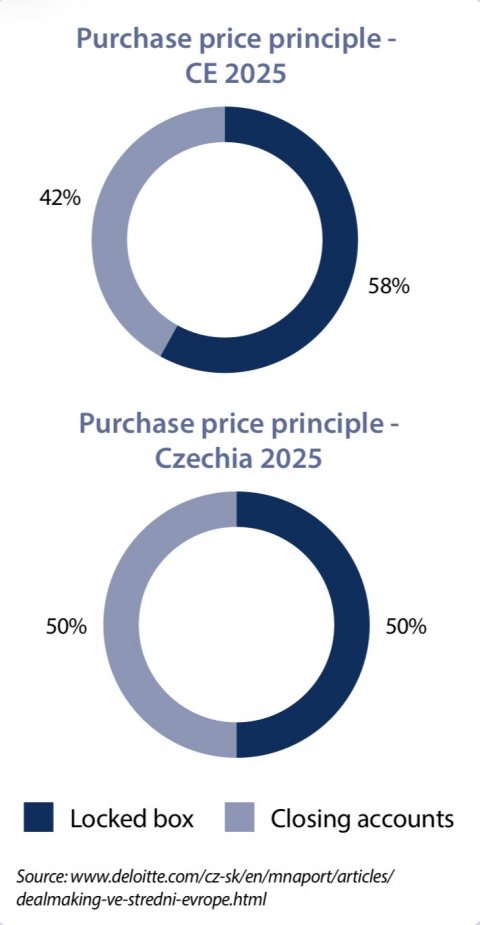

Purchase Price principles

The locked box purchase price mechanism has gained prominence, now featured over 50% of analysed SPAs, reversing the previous significant preference for closing accounts requiring post-closing purchase price adjustment. This shift indicates growing confidence in pre-transaction valuations and reflects dealmakers' preference for price certainty and transactional simplicity. Our previous analysis performed in 2022 showed that locked box was applied in 34% of CE deals and in16% of Czech deals.

The locked box approach offers several advantages, including simplified transactions without the need for special-purpose accounts, greater purchase price certainty, and reduced risk of post-closing disputes. This mechanism is particularly prevalent in smaller markets and for deals of more moderate size, where the benefits of straightforward pricing outweigh the potential drawbacks.

Purchase Price Security Provisions

Purchase price security mechanisms have seen a notable increase. Our analysis reveals that in the Czech M&A market, purchase price escrow, holdback and earn-out are used much more frequently. Compared to three years ago their employment increased significantly.

Warranty Protection and Disclosure

In the Czech legal system, representations and warranties serve as agreed qualities of the target company and form the basis for the seller's liability. To limit their liability, sellers frequently aim to disclose exceptions to these representations and warranties to the buyer.

The Czech M&A market demonstrates a more robust approach to disclosure mechanisms compared to the regional average, as over ¾ majority of deals include the seller's disclosure by referencing a virtual data room, seller's disclosure letters and references to public register disclosures.

Outlook for 2026

As 2026 approaches, M&A practices in Central Europe, including the Czech Republic, continue to evolve and mature. The market is experiencing a gradual shift toward more buyer-friendly terms, provided that thorough due diligence is conducted. For dealmakers, understanding these emerging standards is crucial to structuring transactions that align with current market expectations while safeguarding their specific interests.

|

Petr Suchý |

|