Where to look for an office in Czechia

The office market in the Czech Republic has continued to demonstrate resilience over the past challenging years. Amid the current geopolitical situation, sustainability pressures, and the right-sizing trend, the country is becoming increasingly attractive to foreign investors.

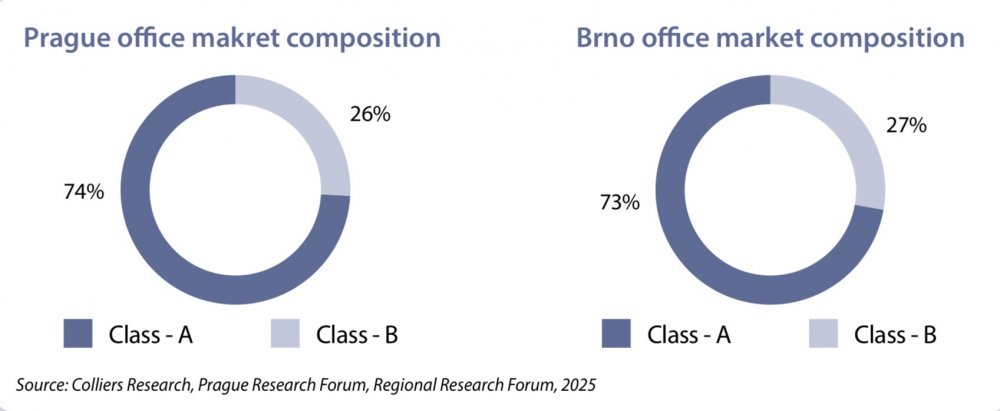

Prague, the obvious choice

When searching for office space in the Czech Republic, the capital is the obvious first choice for many. Many market newcomers are dedicated to establishing the first team here, as Prague is the heart of the country's cultural, economic and political life. The local market comprises almost 4 million square metres of modern office space. Despite lower levels of new office supply over the past five years, developers have delivered a solid inflow of modern properties with high standards and distinctive architecture. Apart from strengthening the market in the most sought-after locations in Prague's historical centre, the Karlín and Rohan areas of Prague 8 and Pankrác and Brumlovka in Prague 4, developers are also establishing new locations with projects such as Roztyly, Hagibor and Smíchov City. Efforts to create a connected city of short distances are also evident and will continue. The vacancy rate in the market remained at around 6-7% and was not significantly affected by any of the challenges faced by other markets. Some micro-locations may have lower office availability, as established submarkets often attract attention for their excellent amenities and well-functioning public transport.

Brno, the leading regional city

Brno is a stable market with approximately six times smaller modern office stock than Prague, but the city does not lack modern office buildings and impressive architecture. The office market is concentrated in and south of the Střed district and the historical city centre, but there are also many exciting projects to the north and east. Newly built office hubs, such as Vlněna, and others form a resilient core for further growth. The office core is supported by extensive industrial & logistics, manufacturing and R&D facilities around the city, which also attract occupiers as well as employees. In the future, we can expect new projects such as Dornych, buildings in the Nová Zbrojovka area, and additions to the Ponávka and Vlněna Office Park. These activities are being carried out mainly by local developers with extensive knowledge of the market and the goal of always providing the highest possible quality and value-added with their projects.

Ostrava and other cities

Ostrava is the third-largest city in the Czech Republic and the country's third-largest office market. Although its modern office stock is relatively small, modern properties comparable to those in Prague and Brno are available throughout the city. Established office centres are home to world-class business service centres and to the newest projects, such as Organica, the latest award-winning addition to Ostrava's office market.

In the rest of the country, local developers are pushing through numerous projects, especially in well-connected cities like Plzeň, Hradec Králové and Olomouc. Such projects, either already existing or in the planning stage, are of high quality and offer excellent services to their clients. Thanks to lower operating costs, choosing to establish offices in smaller cities can prove economically viable but also more challenging to find.

Summary

The Czech economy is on a growth path despite the rest of Europe still trying to overcome recent obstacles. The Czech office markets can attract new tenants and investors through competitive conditions, including high property standards, an innovative environment, and a skilled, well-educated, and talented workforce. Supported by the beautiful, picture-postcard appearance of Czech cities, its high level of safety, high standard of living and its location in the heart of Europe, the Czech Republic should always be on any investor's list of expansion options.

|

Josef Stanko |

|