The Czech tax environment: Transparent and competitive

The Czech tax system is transparent and competitive and offers a number of opportunities to investors.

For individuals

Tax base below 36 times the average salary (approx. EUR 72,000 p.a.) is subject to a 15% tax rate; tax base above this limit is subject to a 23% tax rate. The final tax liability may be lowered by various tax deductions and forms of tax relief, depending on the individual's personal situation.

Participation in the Czech social security and health insurance systems is generally required but can be modified by applying EU legislation or a respective totalization agreement. The Czech social security system covers a wide range of state support, including high-quality public medical care, pension, disability insurance, sickness insurance and unemployment benefits.

For businesses

Business income is taxed at a rate of 21%. A 5% rate applies to basic investment funds. The Czech Republic has transposed the EU Directive on Ensuring a global minimum level of taxation for multinational enterprise groups and large-scale domestic groups in the EU (BEPS 2.0 – Pillar 2) as of 31 December 2023.

The corporate income tax base is determined in accordance with the Czech Accounting Standards, with adjustments for tax purposes. The functional currency is the Czech koruna. A company may choose to use the Euro, the US Dollar or the British Pound Sterling as its functional currency under certain conditions.

Withholding tax is applicable to limited types of payments to non-residents (e.g., dividends, interest, and royalties), however, exemptions based on the respective EU directives and/or double taxation treaties can be obtained.

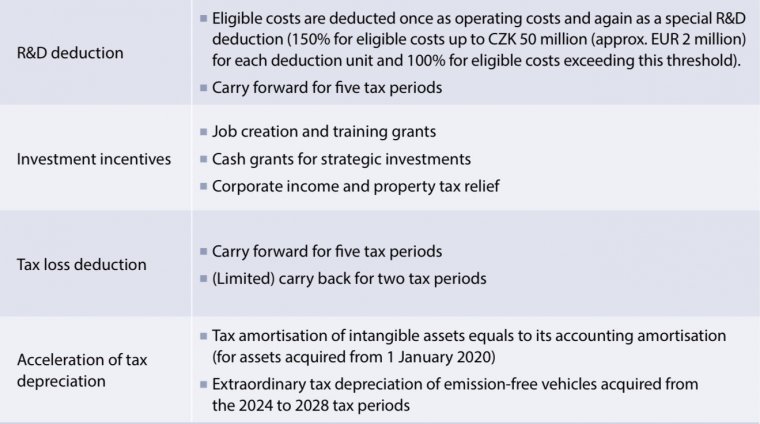

To support the business activities of domestic and foreign investors, the following new and existing benefits are available (see table for more details).

In 2025, some companies active in the energy, oil and banking industries are subject to a so-called windfall tax of an additional 60% on the profits compared to the benchmark stipulated based on the prior years' profits.

Indirect taxes

For VAT payers performing taxable activities, VAT generally should not represent an additional cost.

The standard VAT rate is 21%, and the reduced rate is 12%. Certain supplies are exempt.

The Czech Republic has implemented Directive 2006/112/EC on the common system of VAT and is thus generally in line with the principles applied within the EU.

The transfer of goods within EU member states is generally not regarded as export or import. Goods imported from third countries are subject to import customs duties, excise duties, VAT, and other measures based on the EU customs tariff.

Other taxes

Several rather immaterial taxes such as property tax and road tax for selected vehicles are applicable in the Czech Republic.

|

Radek Matuštík Martin Hladký |

|