Paying personal income tax in the Czech Republic

Czech tax law recognises five types of individual income that are subject to tax and stipulates specific rules for calculating the partial tax base from each of them. The total tax base of an individual is then represented by the sum of these partial tax bases. The personal income tax rate is progressive, with the first rate being 15%. The second increased rate 23% is applicable to income over CZK 1,762,812 (approx. EUR 72,430) in 2026.

Tax residency

Czech tax residents have a duty to pay taxes in the Czech Republic from their worldwide income. An individual is a Czech tax resident if he or she has a permanent home in the Czech Republic or spends here at least 183 days in total per calendar year.

Types of taxable income

The following five general types of income are recognised in relation to individuals:

- employment income,

- business income,

- income from capital assets,

- rental income,

- other income.

Employment income

Employment income is mainly income from performing work based on an employment contract or remuneration of statutory representatives of companies. Tax base is calculated as follows: Tax base = gross salary and taxable benefits (i.e. employment income).

A maximum assessment base applies to social security. For the taxable period 2026, the limit is set at CZK 2,350,416 (approx. EUR 96,580). However, there is no maximum limit applicable to health insurance.

Business income

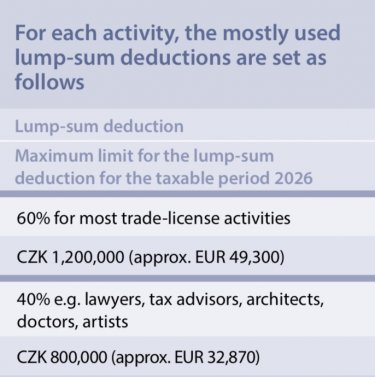

The partial tax base (or tax loss) in relation to business profits is represented by the difference between earned business income and related business expenses. The individual may select the more convenient of the following methods of claiming tax-deductible expenses:

paid expenses in the actual (documented) amount,

lump-sum deduction.

Capital income

Income from capital assets mainly comprises received dividends, interest and income from pension accounts and life-insurance policies.

Rental income

This category includes income from leases excluding some exceptions. The mechanism for calculating the partial tax base (or tax loss) from leases is similar to that for business income (i.e. the individual may choose between claiming actually incurred expenses or claiming a lump-sum standard deduction, which is 30% with the maximum limit of CZK 600,000 (approx. EUR 24,650) for the taxable period 2026).

Other income

Any income other than that described above falls within the scope of the partial tax base, e.g. income from the sale of property or movable assets including shares, from occasional activities and leasing of movable property, non-monetary income, etc.

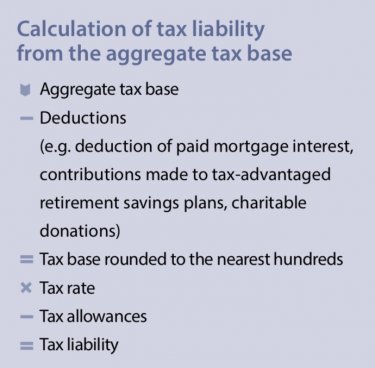

Calculation of tax liability

An individual can also apply deductions and tax allowances, which are applied under the stipulated conditions available mostly to tax residents of the Czech Republic. The tax liability reduced by tax allowances is the final tax liability to be settled with the tax authority. The most frequently applied tax allowances are general annual allowance, allowances for children, and allowances for taxpayers with a low-income spouse (when taking care of a child under 3 years of age).

Tax compliance

The obligation of an individual to submit a tax return arises if the individual has earned taxable income (not subject to withholding tax) in the annual amount of at least CZK 50,000 (approx. EUR 2,050). If the individual has earned employment income only, the related tax obligations are in most cases settled by the employer and no obligation to file a tax return arises.

|

Lucie Bártová |

|