Banking

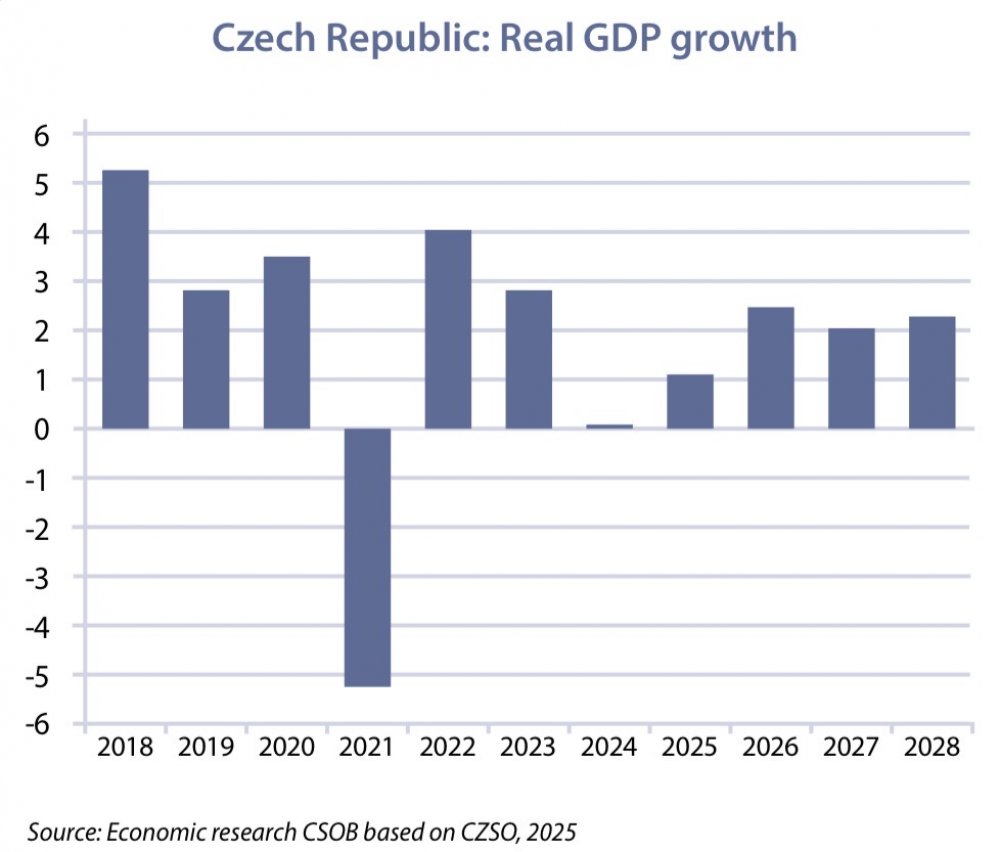

Growth to remain resilient in 2026

After a sluggish post-pandemic recovery, the Czech economy picked up strongly in 2025, with an estimated GDP growth at 2.5%. The key driver remains household consumption, supported by renewed real wage growth and improved consumer confidence. Investment activity and net exports, however, continue to face headwinds from challenging external conditions. The expansion is projected to continue into 2026 at an annual pace of around 2%, underpinned by solid private demand and a more pronounced rebound in investment, aided by lower interest rates and accelerated absorption of EU funds.

The main downside risk for 2026 stems from the external environment and subdued export dynamics. While Germany's economy is expected to recover on the back of higher public investment, uncertainty persists regarding the strength of this rebound. The prolonged industrial downturn in Germany poses a significant risk to demand for Czech industrial output, alongside potential lagged effects of U.S. tariffs and volatile geopolitical developments.

The employment rate remains among the lowest in the EU, yet labour market conditions are gradually easing. This reflects both previous below-potential growth and structural shifts within the economy—namely, a continued reduction in industrial employment and rising job creation in services. Importantly, the unemployment rate at around 3% remains below our estimate of the natural rate, indicating still-tight labour market conditions. Looking ahead to 2026, the overall unemployment rate is expected to stabilize.

Inflation under control

Inflation expectations remain broadly stable in 2026, though price dynamics exhibit notable heterogeneity. Goods inflation is only moderately positive, while services inflation remains elevated at around 4.5% year-on-year, driven by a tight labour market and robust wage growth—estimated at 7.3% in 2025 and projected to ease to 5.5% next year.

Stable interest rates

Against the backdrop of moderating price pressures, the CNB has delivered a cumulative policy rate reduction of 350 basis points since end-2022. It is now expected that the easing cycle is finished, with rates remaining stable through 2026 amid persistent domestic inflationary risks. These include sticky services inflation, strong wage growth, and booming real estate market. This outlook is reinforced by the central bank board's increasingly hawkish tone and its consensus on maintaining policy rates unchanged.

Fiscal expansion ahead

Petr Fiala's outgoing government embarked on the fiscal consolidation path, with the 2025 general budget deficit estimated at 1.7% of GDP — a sharp improvement from 5% in 2021. Both the deficit and public debt (43.6% of GDP) remain modest relative to EU averages. The new government has announced ambitious plans, including significantly higher spending but only limited revenue uplift. Therefore, consolidation efforts are expected to conclude, resulting in a renewed deterioration in public finances. The budget deficit is expected to remain slightly below the Maastricht 3% threshold in the coming years, while public debt is likely to approach 50% of GDP by 2029.

Czech Banking Sector and Economy

There were 43 banks and foreign bank branches operating in the Czech Republic as of 30.09. 2025. The total assets of the Czech banking sector amounted to CZK 11,44 trillion (approx. 467 billion EUR), according to the Czech National Bank.

In 2025, Czech banking continues its shift toward full digitalization, but the focus has evolved. After years of rapid rollout of online functionalities, banks are now prioritizing customer experience and personalization. Instead of adding new features, leading institutions are redesigning digital channels to make them more intuitive and tailored to individual needs. Artificial intelligence plays a key role, powering hyper-personalized offers, predictive financial advice and automated customer support.

In addition, banks in the Czech market continue to strengthen their commitment to ecological and socially responsible practices in 2025. Guided by the Czech Banking Association's Memorandum for Sustainable Finance, institutions integrate ESG principles into their core strategies, applying them not only to internal operations but also to relationships with clients, suppliers, and stakeholders. This includes transparent reporting on environmental and social impacts and active cooperation with regulators and government bodies.

| ČSOB www.csob.cz |