Being an employer in the Czech Republic

Stability with Emerging Structural Challenges. The Czech labour market remains one of the most stable in Europe, yet employers face growing pressures linked to demographic change, digitalisation and the rise of AI. Companies must adapt to shifting expectations, evolving skills and new leadership demands. In this context, organisations increasingly seek leadership advisory to strengthen managerial capabilities and build resilient teams.

According to the Labour Force Survey, unemployment reached 3.0 % in the third quarter of 2025, one of the lowest levels in the EU. Regional differences persist: the highest unemployment was recorded in Ústí nad Labem (5.2 %), Karlovy Vary (4.7 %) and Moravia-Silesia (4.5 %), while Central Bohemia (1.8 %), Prague and Vysočina (both 1.9 %) showed the lowest levels.

Companies continue to struggle with specialised hiring, particularly in IT, engineering, logistics, healthcare and construction. The service sector now employs 62.8 % of the workforce, and part-time work is growing, especially among women, reflecting rising demand for flexibility.

Population ageing increases pressure on employers as the working-age population shrinks. Reliance on foreign workers remains essential, yet administrative processes are lengthy. Succession planning is gaining importance as experienced leaders approach retirement. Insights from Kienbaum's advisory work show that generational transition in key roles is becoming a strategic priority.

Digitalisation and AI are reshaping job profiles and managerial expectations. New roles in data, technology and automation are emerging, while up to four generations now meet in the workplace. Managing this complexity requires modern people practices and adaptive leadership — areas where leadership advisory helps organisations redefine roles and develop leaders.

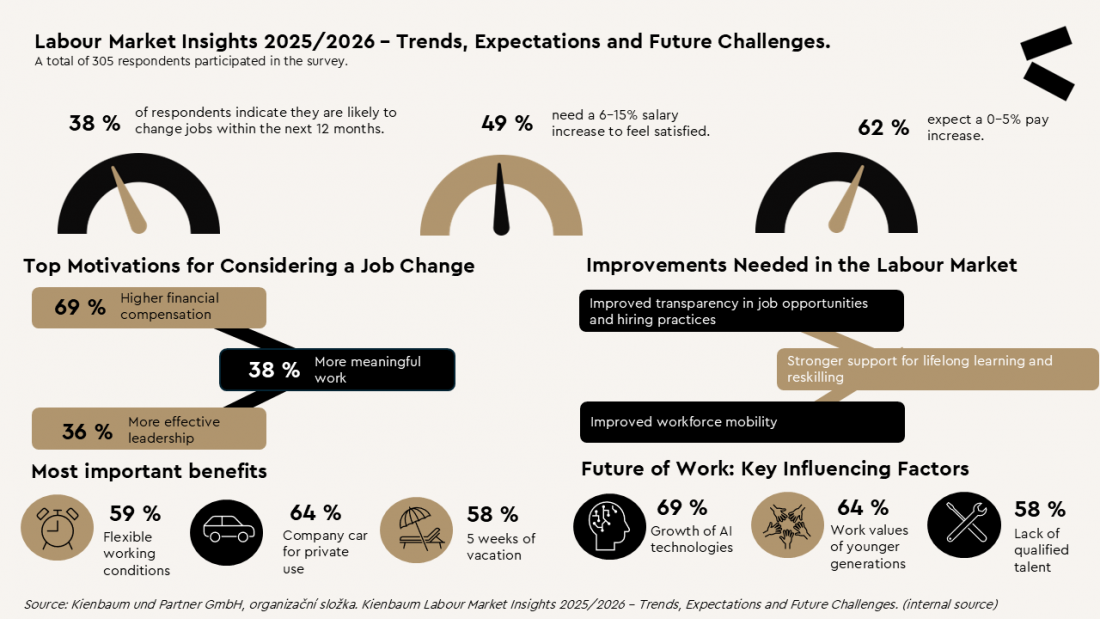

Wages remain a key topic. The average gross monthly wage reached 1,971 EUR in the third quarter of 2025, with year-on-year nominal growth of 7.1% and real growth of 4.5 %. According to Kienbaum Labour Market Insights 2025/2026, 49 % of respondents would need a 6–15 % salary increase to feel satisfied, and flexible working hours remain the most attractive benefit.

Looking ahead, the Czech labour market will depend on employers' ability to attract and retain talent, integrate new technologies and manage generational diversity. Strong leadership capability, talent management and well-structured succession will remain essential in a rapidly changing environment.

|

Jan Nezkusil |

|